Buying a home after the Equifax Hack

Article by Doug Francis https://www.dougfrancis.com/equifax-hack-buying-home-real-estate/

My clients will remember when I said, “Don’t go out and buy his and her BMWs until after you are finished buying the house!” Those days were so simple. Innocent really, almost charming. All that has changed after the recent hack of Equifax essentially exposed everyone’s personal financial information to a remote outpost on the Dark Web… where some dude will make $20 flipping your good name to a cyber gangster. At least they don’t have your 23andMe lab results!

Know these numbers

If you plan to buy a home using a mortgage anytime soon, it’s a good idea to check out your credit report(s). Don’t assume your file is okay – take a look at Equifax, Experian, TransUnion or FreeCreditReport.com . When YOU review your credit report, it does not reduce your FICO Score. If there are old accounts or errors that need correcting, then know it may take a month or two to correct them. Starting today is a smart step that could save you thousands (explained below).

The ideal credit line is one that has aged well. Like a Capital One card that you got in 2003 with a $16,000 credit line and a balance below $5,000 and no late payments. It’s okay, really. The FICO algorithm factors in the ratio of the maximum and actual balance. It’s the ratios that are really important. Ratios are really important. Do NOT close accounts. When you review your credit file, take a look at your account balances because getting them down will improve your score.

Two-Step Authentication

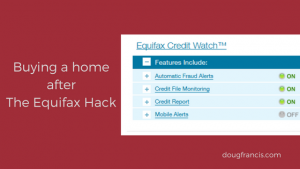

A smart step is to set up a two-step authentication on your credit. Which means, when you apply for any new credit, mortgage, car, furniture, and possibly insurance, Equifax will need to contact you and confirm with you first in a manor you have instructed them to ahead of time. Yes, they will even call you. It’s like when Microsoft or Google texts a code to you when you log in from a new location.

I set this two-step process up on my Equifax account about ten years ago after reading an article in BusinessWeek. It seemed smart especially since I have published a ton of personal information on the Interwebs. It was also when I decided to get serious about managing any credit balances and hold myself accountable like I was preaching to my clients.

At that time, I added the Automatic Fraud Alert to my account. You should do this too. The Automatic Fraud Alert requires Equifax to contact me when I apply for new credit. For example, when I bought my VW TDI (that’s another dark story) I was contacted by Equifax and required to confirm my identity with a PIN. After VW bought back my super-polluter TDI, I bought another car triggering the same two-step authentication. Maybe it is a freeze on my account, but hopefully, it makes my credit a little harder to hack.

The FICO Score is baked into our lives.

The FICO Score is baked into the life algorithm of America. FICO Score what lenders use. Want to finance a car? Your rate depends on your FICO Score. Looking for a new job? They will look at your FICO Score. Hoping to get a mortgage? They will look at your FICO Score.

The role that Experian, TransUnion, and Equifax play is monitoring your open credit lines, payment history, and ratios. And they have information such as your previous addresses, current and past employer, and any criminal activity (including unpaid parking tickets or Court convictions). All that information gets plugged into the FICO Score algorithm generating a number ranging from 300 to 850. You want a high number. That FICO Score will 100% determine what happens to you and how much you pay for a wide variety of things. FICO is totally baked into the U.S. financial system.

Home Buyers… Start Here

When you are buying a home and are working to get a mortgage, you really have to control what you do. Such as not buying new BMWs, adding a new line of credit at Ethan Allan, or saving 20% at Target with a new Target Card. Any new credit line additions are really bad decisions, and break Doug’s Prime Directive for buyer clients. Mortgage lenders pull your file when you apply for your loan. But, it is critical to know that the lender will pull your credit one more time just before Settlement. If you have added any new credit or a fake account shows up… then they will see it. And, your FICO Score may be impacted.

Start right now:

look at http://www.equifax.com/

look at http://www.experian.com/news/data-breach-five-things-to-do-after-your-information-has-been-stolen.html

look at https://www.transunion.com/equifax-data-breach-faqs

When you apply for a loan, your mortgage lender will ask for permission to review your credit. They order a tri-merge credit report seeing all three reports, and see your FICO Score.A higher FICO Score will allow the mortgage people to offer you a better rate saving thousands of dollars every year. That is why I want you to spend time now taking the effort to improve your score.

Example:

$500,000 loan amount at 3.75% on a 30 year loan has a Principal and Interest payment of $2,315 vs.

$500,000 loan amount at 4.25% on a 30 year loan has a Principal and Interest payment of $2,460

After 30 years… that’s $52,200 more!

So, I hope you understand why it is really important that you check your credit file and your FICO Score especially if you are planning on buying a home. The myth that pulling your credit negatively impacts your score is wrong, totally wrong. When you review, check for errors, you will see easy opportunities where you can improve your debt ratios.

With a little work now, you will improve your ability to buy a home in 2018. –author Doug Francis https://www.dougfrancis.com/equifax-hack-buying-home-real-estate/

Recent Comments